If you care about Open Banking, you want to download this March ’21 Open Banking Landscape research report.

I’m endlessly curious about this space, but feel that many people/companies do a great job explaining what open banking is, but fall short when it comes to understanding the drivers and market forces.

If you define opening banking and talk about banks and data sharing, you’re missing the ‘why’.

Screen scraping

Banks already share data. Unwillingly, so unwillingly that they have teams fighting the current method of data sharing: Screen Scraping (if you want to read something about screen scraping that's not written by me, read this), and are suing Plaid who’s built a business on screen scraping bank data.

Moving from Screen Scraping to APIs is in the bank’s interest, and an important step, but it’s doesn’t address the underlying shift. The underlying pressure for doing so.

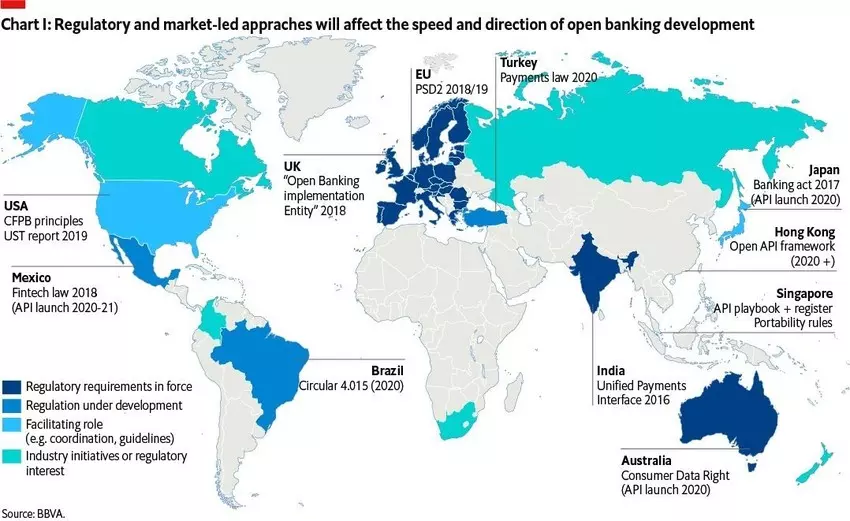

Sure, while in Europe and elsewhere there are regulatory pressures to open up, that pressure originates in the customer.

Actually, in Europe that pressure originates from the cultural perspective on privacy and the manner in which governments support that perspective through regulations. Left to their own devices, it's unlikely banks would open themselves up, even to the benefit of their customers.

What’s the ‘why’?

It’s the same why that drove GUIs vs command line computer interfaces. Technical people were fine with command line. In order to expand the market, GUIs made it easier for regular people to use computers to solve their own problems.

The driver for open banking is the customer. Some customers can navigate banking services, but few have a good way to track their financial wellness. Making it easier to share data, enables solutions that provide a higher-level valprop solving the actual job customers hire banks to do.

By example, when speaking I'd often ask who wants to be in half-a-million dollars of debt? Surprisingly, no one ever raised their hands. Yet, if I asked who wanted a home, where they could set down roots and raise a family... most every hand in the room went up. No one wants a mortgage. They want to buy a home. And so on.

While I really like this research report, on page 6 where they give an overview, they only talk about banks and their customers. They don’t talk about customers and their banks. This is subtle.

Customers don’t want their data. They want better financial tools (that use their data).

This will also help big banks with their internal business cases. It’s much more compelling to create an open banking business case when you describe customers who want better financing solutions (perhaps by sharing data with Affirm) than by saying something like “Affirm wants our data to compete with our lending practice”. Both of those things may be true, but if you understand the customer, you can use open banking to compete better as opposed to giving away the crown jewels to fintech competitors.

Anyways, read this, then look at page 6 again. Customers don’t want “ownership of data back into their own hands”… they want improved financial wellness..

A bank that just opens data because that’s what customers want… will be giving it all away.

A bank that understands what customers want, and realizes the opportunities enabled by opening customer data will be a winner.

It’s the same but different… at first Amazon lets anyone sell on their site. Then, they watch customer behavior, create Amazon Basics versions, and win.

Why wouldn’t this be a viable strategy for a bank? After all, banks think they’re software companies with banking licenses.

More nuggets

- Page 7, right column has some good bullets on the benefits of open banking. I particularly like the term “embedded finance”. In looking through my notes for things I'd like to write about, coincidentally I came across this tweet about a McKinsey report identifying six embedded-finance trends:

Increasingly, financial services firms are incorporating embedded finance to provide value to their customers. @McKinsey identifies six trends to watch out for, and key considerations for firms wishing to expand their embedded finance offerings. https://t.co/LKarmGNex3

— DriveWealth (@DriveWealth) March 11, 2021

- Page 12 has a great breakdown of the forces driving global open banking initiatives. (Again though, this is mostly from the bank/regulatory perspective, not from the customer perspective.)

- Page 14 finally mentions personal finance tools and the customer’s behaviors. This is probably a good time to mention that banking is way more than retail and consumer credit card banking (though that’s what we’re all familiar with as humans). Banks have been providing solutions to enterprises for a long time, solutions that could benefit by being more open than they are today. And, then there’s also DeFi where integrating between legacy banking infrastructure and crypto-banking infrastructure is going to be a multi-decade effort.

- I disagree a little with the conclusions presented on page 16. Consumers may, for example, be worried about identity theft. But, are they at any additional risk of identity theft than without open banking? And, is it really the customers who worry about these things, or the banks who bear much of the costs? Color me skeptical. For that identity theft stat, 69% of customers are concerned, still leaving 31% of customers open to the innovations! That’s a huge market, even if that were a rock-solid show-stopper for 69% of customers. In fact, I’d bet that the people willing to take the risk on new services are often the most profitable… so you’re willing to lose your best customers to innovative solutions delivered by your competitors rather than deliver the innovation yourself for a small-is segment of your overall customer base? Why don’t you ask your customers if they want products targeted at the lowest-common denominator of your entire customer base, or do they want leading edge solutions to their problems? Even if they don’t have any specific problem today, higher end customers like to know that their financial partner has the solutions they need when the time comes.

- Page 18 and on has a great collection of stories and solutions. Amazing! There’s some really great data and stories presented in here that’s worth digging into.

Final thought

Any time APIs are brought up without a mention of security or developer collaboration, I’m sad.

This space is so mature, and yet companies still think they want to create their own security stack, or integrations with their entire security infrastructure.

Or, they want to drive a whole new generation of banking business, but they’ll create a developer collaboration tool using something free and cheap because someone wants to throw the IT staff a bone and let them have a decision (in my day, we just got pizza and were expected to be compliant).

It’s inevitable that security will change over time. You want a product that abstracts security out of the solutions you create so that it can be managed by the right team, without impacting application deliverables and slowing application releases down.

It’s inevitable that you’ll have your own APIs, have APIs you share internally, with partners. That you’ll have many different platforms with APIs (like AWS, Azure, etc). You probably have legacy solutions (like Broadcom/CA or Apigee).

You need the best security, with the right over-reaching governance and collaboration, even across legacy piecemeal solutions purchased years ago, in a very different market.

In my experience, the best solution to help with this aspect of Open Banking is Axway. The analysts (Forrester, Gartner) agree too, though while they don’t pick one winner I can.

Anyways, check out that report it’s incredible. Then have a look at Axway’s open banking solutions for API security and collaboration (or follow their Open Banking podcast). Even if you already have an API collaboration tool, Axway works with all the big players to provide a single, secure, platform for the future of open banking, fintech, and DeFi.

Update April 6, 2021

The World Economic Forum released a report titled "What's next for Open Banking". It's a good overview, and has some interesting links if you want to head down the rabbit-hole.

Interestingly, two of the key points are that the appetite for open banking is growing globally and banks aren't digital enough. One might conclude reading these points that banks aren't up to the task that customers are hiring the industry to deliver. Maybe that's why out of nowhere a company can show up on the scene and be one of the largest banks on the planet practically overnight.

Separately, I saw this interesting article talking about the "business benefits" of embedded payments. Above, I wrote about embedded finance in abstract, so this real-world example caught my attention.

I've talked about the value of embedded finance in the past. At a story-level, it's about bringing the bank's "processes" to the customer, instead of asking the customer to come to the bank. Why leave the coffee shop to go to the credit card, when you can have payments right in the coffee shop app? Same for mortgages (Zillow), or loans (Affirm).

Update May 11, 2021

For a while I'd talk to customers about "unbundling banking" into composite services that become their own market based on the experience around that service.

Service providers (banks, neobanks, fintechs) can narrow their offering, deliver an outstanding experience, and most importantly, take the profitable customers from the conglomerate banks that want to homogenize everything.

We see this happening across the spectrum of banking services. That's why this tweet and the attached image caught my attention:

"Fintech hasn't unbundled banking. Fintech has atomized banking."

— David Bentzon (@david_bentzon) May 11, 2021

It's a very useful lens to view the current landscape. https://t.co/MXeXnZso3s pic.twitter.com/BSGkQXXQtV

I don't know if there's a lot of nuance between unbundling banking and atomized banking, or maybe it's just how I think of it. To me it seems two sides of the same coin. I agree that banks have no idea what's coming. And perhaps that's why they're going to face a tough decade ahead?